Wealth Protection

Why should I buy life insurance?

1) Replace income for dependents If people depend on your income, life insurance can replace that income for them if you die. The most commonly recognized case of this is parents with

young children. However, it can also apply to couples in which the survivor would be financially stricken by the income lost through the death of a partner, and to dependent adults, such as parents, siblings or adult children who continue to rely on you financially. Ins

urance to replace your income can be especially useful if the government- or employer-sponsored benefits of your surviving spouse or domestic partner will be reduced after your death.

2) Pay final expenses

Life insurance can pay your funeral and burial costs, probate and other

estate administration costs, debts and medical expenses not covered by h

ealth insurance.

3) Create an inheritance for your heirs

Even if you have no other assets to pass to your heirs, you can create an inheritance by buying a life insurance policy and naming them as beneficiaries.

4) Pay federal “death” taxes and state “death” taxes

Life insurance benefits can pay estate taxes so that your heirs will not have

to liquidate other assets or take a smaller inheritance. Changes in the federal “death” tax rules between now and January 1, 2011 will likely lessen the impact of this tax on some people, but some states are offsetting those federal decreases with increases in their state-level “death” taxes.

5) Make significant charitable contributions

By making a charity the beneficiary of your life insurance, you can make a much larger contribution than if you donated the cash equivalent of the policy’s premiums.

6) Create a source of savings

Some types of life insurance create a cash value that, if not paid out as a death benefit, can be borrowed or withdrawn on the owner’s request. Since most people make paying their life insurance policy premiums a high priority, buying a cash-value type policy can creat

e a kind of “forced” savings plan. Furthermore, the interest credited is tax deferred (and tax exempt if the money is paid as a death claim).

Source : Insurance Information Institute

How much life insurance do you need?

This refers to the amount of life insurance death benefit that is needed upon a person's death. When a person passes away leaving the loved ones behind there would be loss of income and that is why life insurance is required to replace for the loss of such income. The emotional loss of a loved one will never be replaceable but at least the financial part of the loss can be covered by sufficient life insurance protection.

How much life insurance is needed for the breadwinner of a family?

To simplify the illustratin, assuming that the husband of a family is a wage earner or breadwinner. The wife may or may not be a wage earner.

1. Estate liquidity

Extra cash may be needed immediately after his death- Need to make mortgage repayments

Need to pay other debts

2. Expected medical bills not covered by his medical insurance policy

Most people do not pass away in an accident. Instead, a person usually passes away due to

some kind of disease or illness. Hence, it may be expected to have accumulated a certain

amount of medical and hospital expenses before he passes away. And this amount to lifeinsurance death benefit requirement. Otherwise include a medical benefit into his life

insurance policy that provides hospitalization and surgical benefits.

3. Needs for children's future education

4. Fall in family incomeIf he is a breakwinner, his family income will be reduced when he passed away.

5. Sole proprietor business or partnership

6. Reduction in family expenses

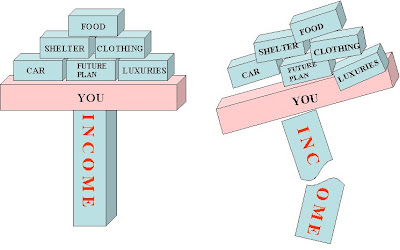

Every Person in this world will face the same situation

a) Die too young - Broken Dreams. Unfinished Plan. Family lost the support.

b) Die too old - Staying alone. Unable to suport ourselves.

c) Total & Permanent Disablement - Unable to support the family. Children not able to study. Depend on charity.

d) Dread Disease - Large amount of medical fees. Mentally & physically suffered. Unable to support the family.

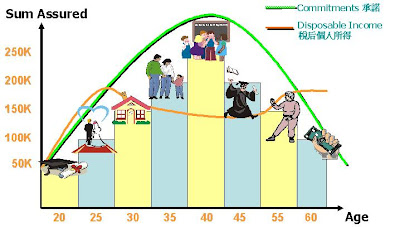

Flexible Protection Curve

In life, we have different concerns and financial goals at different stages.

You ----> want to enjoy and

maintain your lifestyle, so you need...

Income $$$ - to support your lifestyle, if your income pillar collapse, you may have broken dreams.

To secure your current lifestyle, we will help you to plan your future financial needs '3 pillars' to ensure you can maintained all your dreams.

{kind=link}